Central de Notícias

Sinais de mercado, documentação de comércio e insights de compra para importadores de açúcar do Brasil. Dados verificados, sem especulação.

NEWSLETTER

NEWSLETTERNewsletter

11 publicaçõesAtualizações periódicas sobre mercados de açúcar, janelas de laycan, SGS e instrumentos DLC/SBLC.

Comércio Internacional

Comércio InternacionalComércio Internacional

6 publicaçõesDicas de documentos, amostras COA/SGS, checklists UCP 600/URC e playbooks de embarque.

APRENDER

APRENDERAprender: Economia & Finanças

10 publicaçõesGuias de mercado: basis vs preço fixo, frete & câmbio, e sazonalidade de custo entregue.

Newsletter

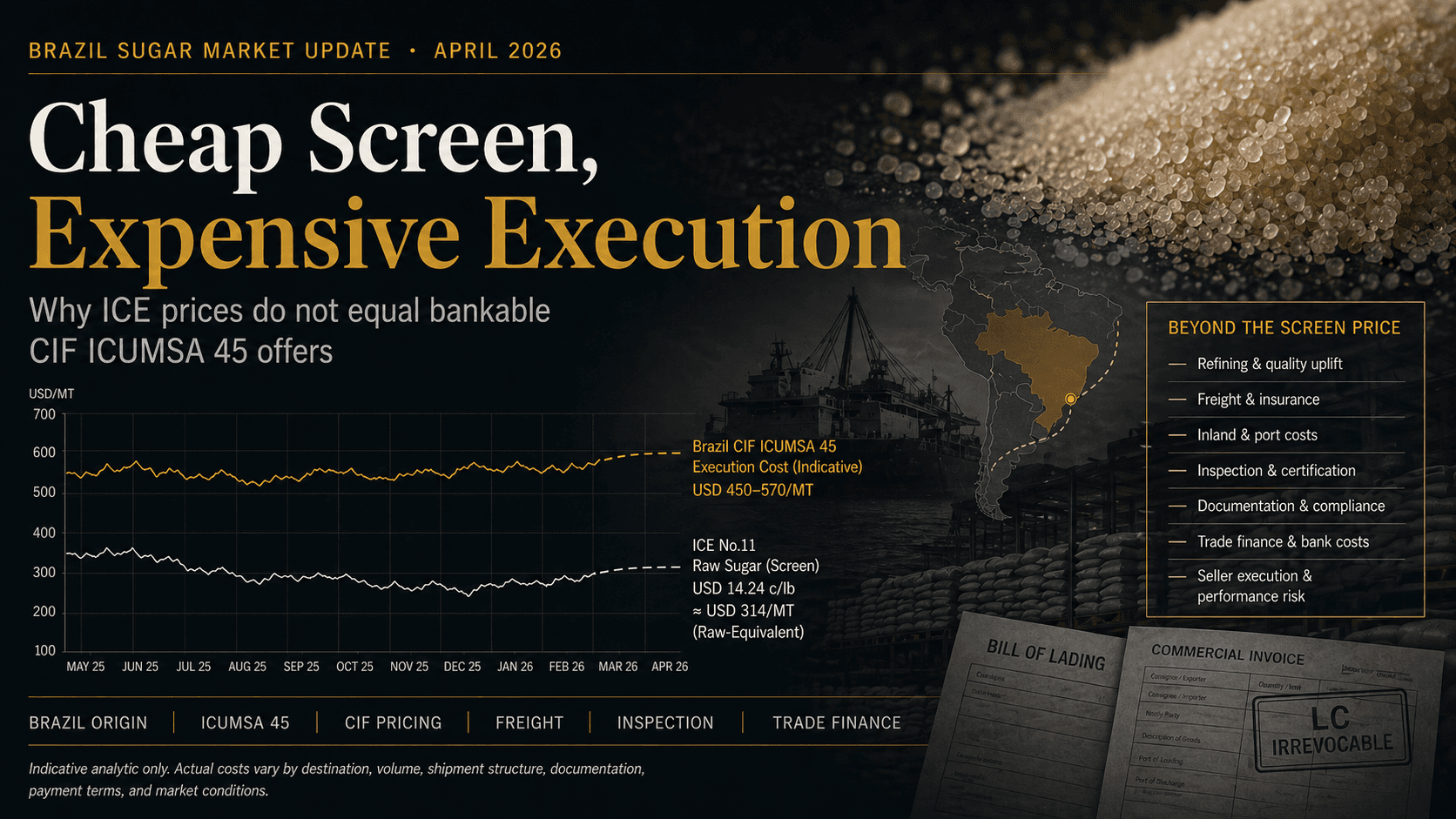

Brazil Sugar Market Update for April 2026

ICE sugar prices may look cheap, but Brazil-origin ICUMSA 45 CIF execution tells a different story. This update breaks down the real cost stack—refining uplift, freight, inspection, and trade finance—and explains why serious buyers must look beyond the screen.

Brazil Sugar Market Review — February 2026

Brazil’s off-season exports surged 44% above year-ago levels while ICE No. 11 raw sugar futures fell toward 14 c/lb amid growing global surplus expectations.

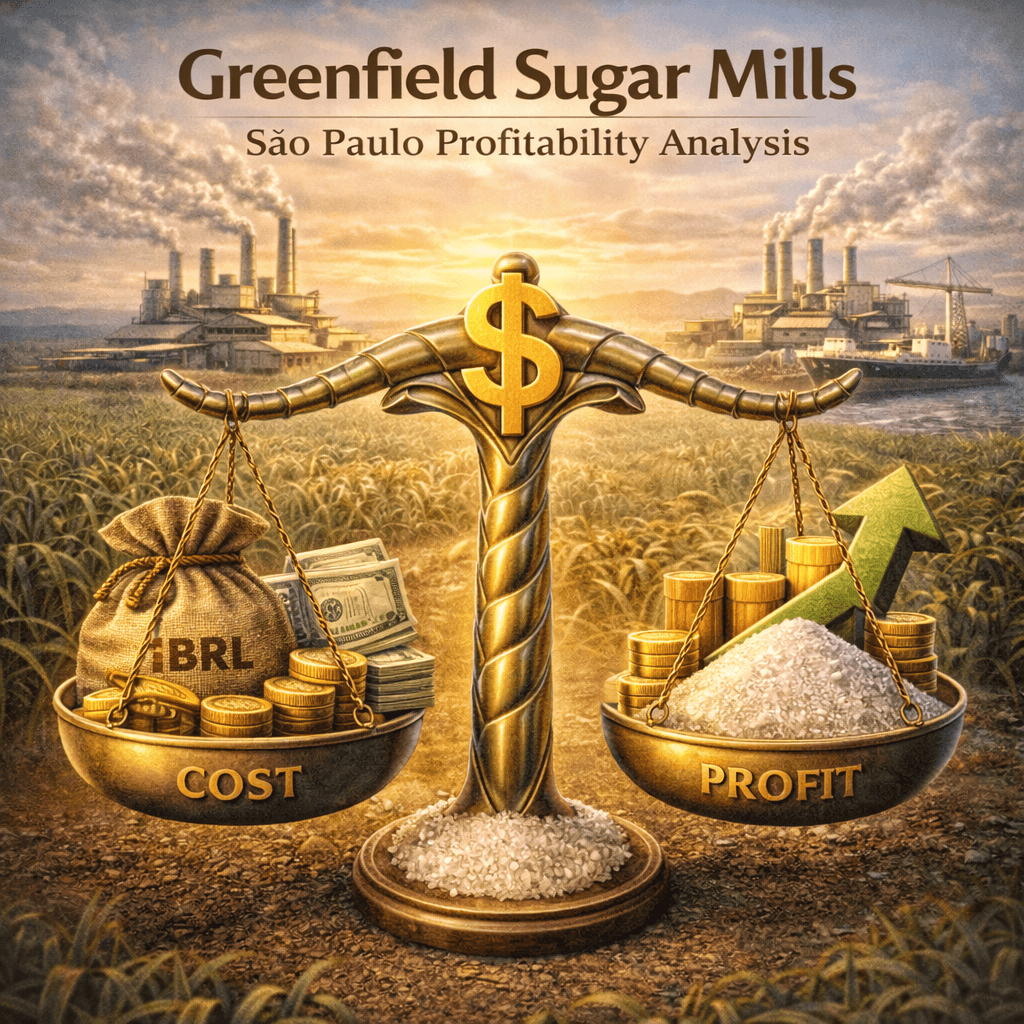

Sugar Mill Unit Economics in São Paulo: The Margin Stack From Cane to FOB

Greenfield sugar mills in São Paulo can work, but profitability is brutally sensitive to sugar price, ATR-linked cane cost, FX, and scale. At mid-cycle pricing, a 3M t/year mill can generate roughly R$150–R$200 EBITDA per ton of sugar FOB, while smaller mills hover near break-even and mega-mills win on unit costs and co-gen uplift.

Comércio Internacional

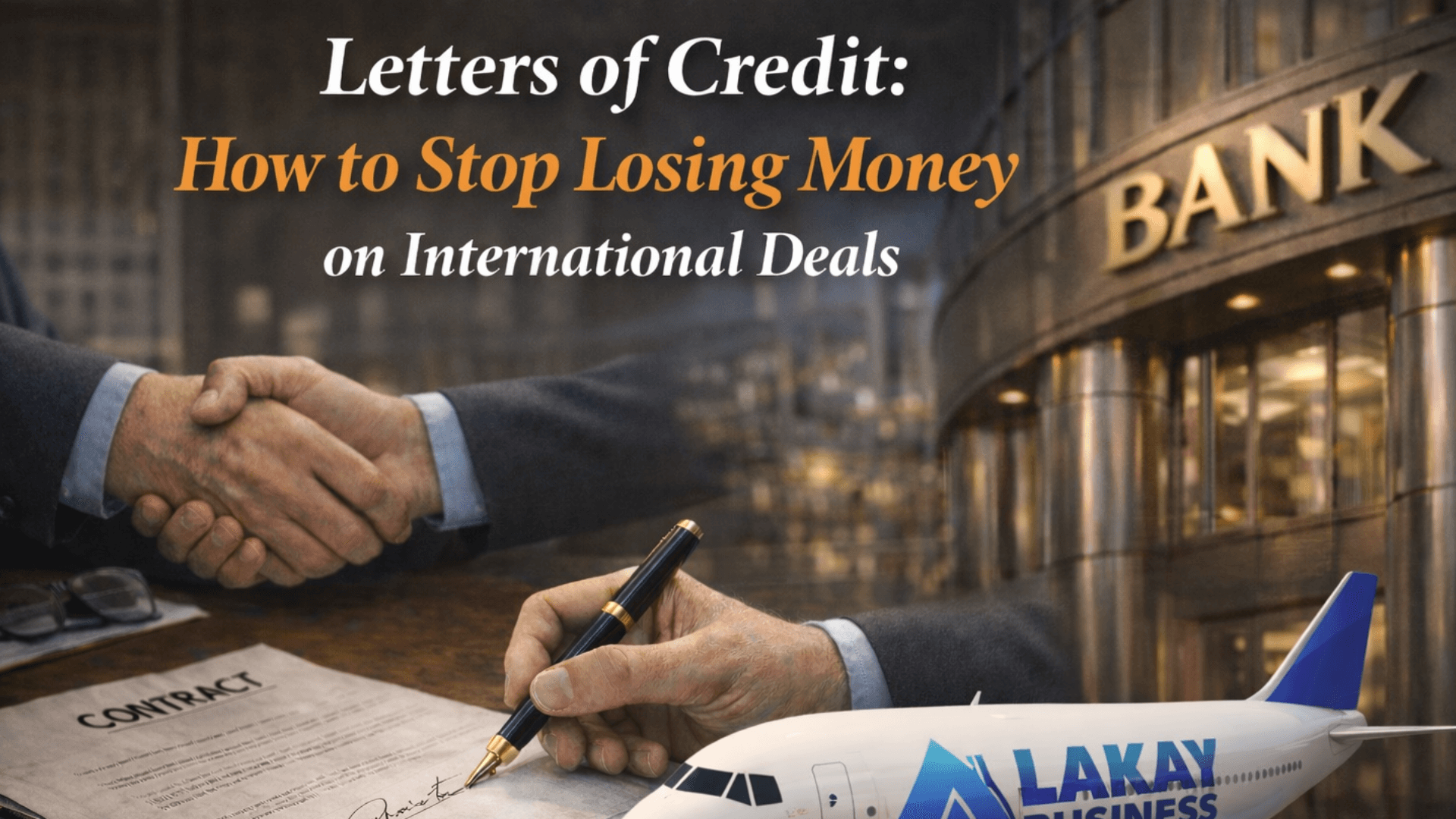

Why Letters of Credit (LCs) Still Rule Global Trade Finance

Letters of Credit still dominate trade finance because they solve one thing better than anything else: trust. Learn how LCs work, how they compare to SBLCs, and the best practices to avoid costly mistakes.

Trump's Secret War on Brazil

The 50% tariff on Brazilian imports in July 2025 wasn’t the opening shot—it was the closer. Publicly, the White House billed it as hardball over “unfair practices.” Privately, it capped a years-long, multi-front squeeze designed to pry Brasília away from Beijing: reciprocal-tariff powers, targeted trade cases, and pressure campaigns that bled from steel to 5G. The tariff itself is on the record; the wider playbook—phantom financing offers, leverage built from crises, and a carrot-and-stick tech strategy—emerges from leaked files and off-the-record briefings. The result? Collateral damage at home and abroad, plus a strategic own goal: rather than isolating Brazil from China, the squeeze hardened Brasília’s hedging instincts and deepened regional skepticism about Washington’s reliability. What looked like a tariff tantrum reads, in full, as a modern shadow war—economic instruments wielded in the open, coercive tactics in the dark—and a case study in how decoupling gambits can boomerang.

Navigating the New Trade Landscape: How U.S. Tariffs Are Reshaping Brazil’s Economy

When Washington’s tariff wall went up, Brazil’s farm belt felt the tremor first. In Mato Grosso, João Silva’s soy turned into overnight gold as Chinese buyers pivoted away from U.S. supply. The surge is real—but fragile. Brazil is benefiting from trade diversion: soy, corn, and beef bookings swell while steel and aircraft stare at headwinds. A “baseline” U.S. tariff stings less than China’s higher rates, yet the bigger risk is strategic: over-reliance on a single customer and a global slowdown if the spat drags on. Brasília’s play is threefold—negotiate exemptions, keep a calibrated retaliatory stick ready, and sprint on diversification (EU, ASEAN, others). Internally, tax relief and logistics upgrades aim to lock in farm gains without torching consumer prices. Net-net, the shock is bad in the absolute, potentially positive for Brazil in the short run. But João’s wife has a point: windfalls born of geopolitics can disappear as quickly as they arrive. The winners bank cash, hedge exposure, and build markets beyond the current crisis.

Aprender: Economia & Finanças

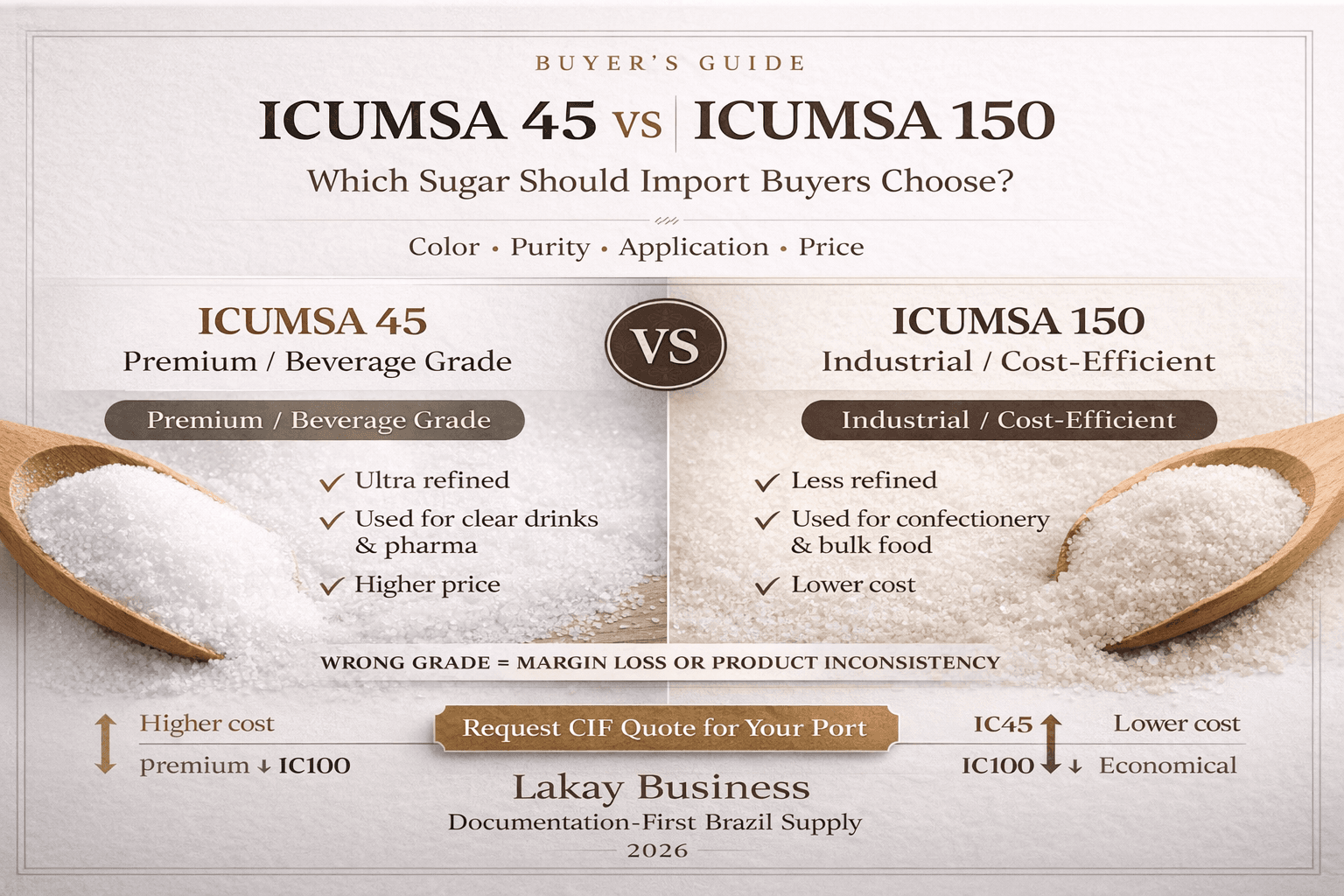

ICUMSA 45 vs ICUMSA 150: What's the Difference for Import Buyers?

Compare ICUMSA 45 and ICUMSA 150 sugar for import buyers. Learn the key differences in color, market fit, pricing logic, and contract checks before choosing the right grade.

What Is ICUMSA 45 Sugar?

The Complete Buyer’s Guide Specifications · Trade Execution · Documentation · Payment Structure · Risk Management Lakay Business | lakaybusiness.com | 2026 A publication-grade reference for commodity traders, importers, food manufacturers, procurement teams, and trade finance professionals.

Global Sugar Market Outlook | Q4 2025

The Q4 2025 sugar market looks “cheap” on the screen, with ICE No. 11 near 14.8 c/lb, even as ISO projects a 4.9 MMT global deficit and Brazil runs at record sugar exports. This note explains why the market is mispricing risk and sets out a Brazil-anchored 50/30/20 coverage strategy for protecting 2026 margins.

Pronto para comprar?

Da inteligência de mercado a cotações CIF firmes — nossa mesa está pronta.